Louise emerged from the bank branch and performed a spontaneous happy dance.

Passers-by gave her worried looks and a wide berth. The only people who were ever that happy are either young children, drug-addled, mentally ill or ultra-religious.

Louise had just paid off her mortgage. Eight years early.

After a marathon seventeen years of hard graft. Scrimping and saving every spare penny in a determined effort to become debt-free as soon as possible. A homeowner in the true sense of the word.

Twenty years ago, Louise had been a high flyer in the technology world.

She hadn’t jumped aboard the freelancing gravy train as many of her colleagues had done. Too risky.

Instead, she stayed loyal to her employer. Worked hard. Did all that was asked of her and did it well.

Her reward was to be TUPEd to a global service provider, when her employer outsourced their technology function. Not a core function. Non-essential staff.

Pension slashed.

Benefits eroded.

Spirit slowly crushed beneath the corporate realities of a “do more with less” mantra.

The outsourcer had a profit margin to defend. Louise was comparatively expensive for her skillset.

Her daily existence came to resemble an attritional game of chicken with an oncoming train. The outsourcer wanted her gone because she was too expensive. Louise wanted a redundancy payout.

Eventually, she blinked first. Life was too short to spend the better part of each working day feeling miserable and exploited. To waste her weekends silently dreading the approach of Monday morning.

Louise quit. Quit the outsourcer. Quit the technology game. Quit London.

She went back to school and retrained as a nurse.

Financially the move was an own goal, but she was performing work that she felt was meaningful and added value.

Some of the patients she helped even said thank you. Occasionally. The computers she once fixed for a living never did that.

Conventional wisdom is wrong

Louise becoming debt-free was a commendable achievement. Particularly given the criminally low wages that nurses receive for the valuable work that they do.

Yet I can’t help thinking that Louise had scored another financial own goal by doing so.

Conventional wisdom says that all debt is bad.

However, as is so often the case, conventional wisdom is wrong.

Becoming debt-free is a powerful psychological safety blanket. Similar to the night light that keeps a young child’s dreams safe from imagined monsters hiding in the darkness.

Being scared of the dark is an irrational fear. So too being scared of debt.

Counterintuitive though it may seem, the careful use of debt can help us realise goals that would be impossible to achieve any other way.

Less irrational fear, more a case of choosing the right tool for the job.

Debt often gets conflated with the sensible sounding notion that if you can’t afford to pay cash for something, then you probably can’t afford it at all. This holds true in the context of foolish consumer debt like car leases, credit cards, and mobile phone plans. It misses the mark when debt is used to finance investment goals.

Many of us routinely deploy debt to help realise our goals.

Investing in our future earning potential via studying is one of the most powerful investment decisions we can make. Even if it means taking on student debt to do so.

Providing we make sensible choices about the future employment prospects for our chosen field of study, that investment will pay for itself many times over. The compounding returns achieved by increasing our earnings potential will be the most successful investment many of us will ever make.

Some students choose poorly. Running up debts studying disciplines that are unlikely to ever pay for themselves. Falling into the status-seeking trap of purchasing luxury branded degrees from expensive institutions. The cost/benefit outcome from these borrowing decisions can be disastrous.

A common definition of financial independence is living in a paid-off home and having enough additional savings set aside to sustainably cover the costs of leading a comfortable lifestyle.

Yet how many people can afford to pay cash upfront to purchase their home outright?

Not many.

The rest of us take on debt in the form of a mortgage, to help us realise the dream of owning our own home. As time passes, and repayments are made, that debt reduces just like it did for Louise.

In the United Kingdom, homeownership is heavily tax-advantaged. Unlike other assets, we pay no capital gains tax on any increases in the value of the property, providing that we live in it.

If we are comfortable borrowing to enhance our future wealth by investing in education, and we barely pause before borrowing to enhance our future wealth through homeownership, then why are many people scared of borrowing to enhance their future wealth via investments?

This is a curious behaviour. Emotionally it may make sense. From a logical perspective, it is irrational.

Case study

Consider Louise’s paid off house as an example. She now has a house that she owns outright. However, all that hard-earned equity is effectively trapped and generating no income. Any capital growth the house may experience is only accessible if she were to sell it and move someplace else.

An alternative approach would be to take out an interest-only offset mortgage or line of credit.

Let’s imagine Louise drew down the principal of the loan and deposited it all in the offset account. She would incur no interest charges, as the loan balance minus the offset account balance would be £0. Financially she is in the same position that she is today with her fully paid-off house.

Now let’s imagine Louise identifies an attractive investment opportunity.

She can pursue that opportunity using funds from the offset account.

Louise would only pay interest on the amount of money she drew down. Providing the investment return exceeded the interest charges on the loan, the investment would be self-financing.

To illustrate, consider a simple case study.

At the time of writing Coventry Building Society offers a 25 year offset mortgage with a variable interest rate of 2.19% per annum.

The Vanguard FTSE All-World High Dividend Yield ETF (VHYL) had a dividend yield of 3.66%.

If Louise used borrowed funds to purchase VHYL shares, the investment would be generating excess cash flow of approximately 1.47% after covering the financing costs. She may also have to cover brokerage charges and taxes, though increasingly these days both are becoming optional.

In addition to the cash flow, those shares may increase in value over time. This is capital growth Louise would not have enjoyed had she simply paid off her house. Of course it is worth remembering that shares could fall in value rather than rise. There is always risk associated with potential reward.

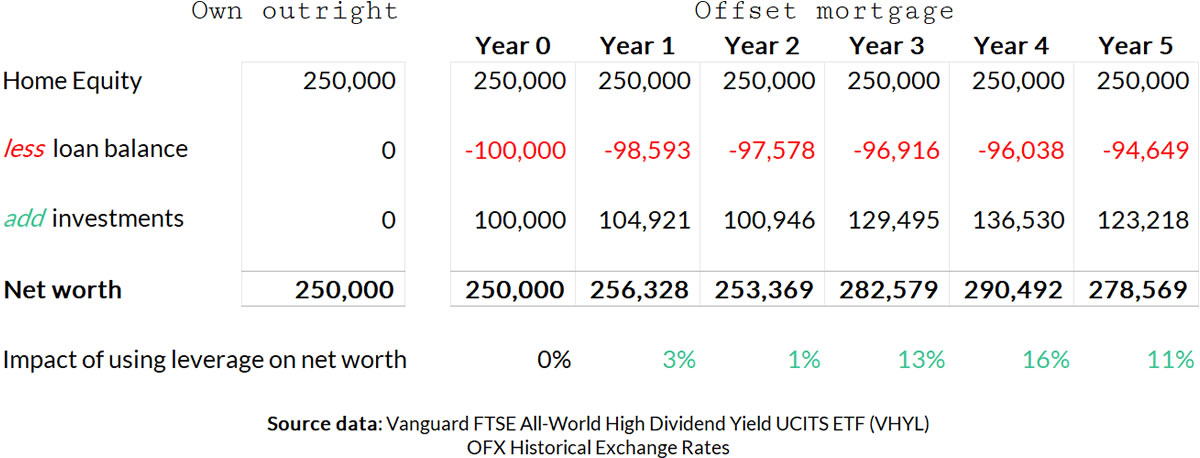

To bring that to life, the table below outlines how this approach would have performed for Louise over the last 5 years.

It would have been a rollercoaster ride, but financially Louise would be better off.

I have deliberately selected the High Yield ETF for this case study because the cash flow it generates covers the interest payments on the loan, and because it has experienced ups and downs that reflect the vagaries of the stock market. In reality we should always consider total returns when evaluating investments, as chasing short term yield often results in missing out on long term growth.

Interest only

Case studies and contrived outcomes are easy to pull together in support of virtually any argument. The approach I’m suggesting Louise consider isn’t just a hypothetical thought experiment. Rather it is a technique I have been successfully using for many years.

When I was 23 years old I bought a house.

Four bedrooms. Two and a half bathrooms. 3000+ square feet of living space. Double garage. Front and back yards.

It was a brand new house. In a brand new subdivision. Opposite a brand new park.

A bit of research at the local government’s planning office had revealed plans to construct nearby a new shopping precinct, primary school, high school, football stadium and motorway to the city centre.

All would significantly boost the neighbourhood’s desirability, employment, and property prices.

I paid the purchase costs and 10% deposit in cash. That felt like a lot of money at the time.

The rest I borrowed via a home equity line of credit. No loan term limit. No set repayment schedule. Providing the loan limit wasn’t breached, the bank didn’t care whether I made repayments at all.

I hired a property manager. They found some good tenants. The rent more than covered the financing and holding costs. Gradually the tenants paid down the outstanding loan balance.

A couple of years later I drew down on the line of credit again, using the funds to pay for the deposit and purchasing costs of another property. This time I contributed no cash to the deal.

Once again I hired a property manager. They found some tenants. The rent more than covered the financing and holding costs.

Rinse and repeat.

That interest only lending facility has enabled the purchase of a half dozen properties over the years.

Today I still own that first property, and it still secures a line of credit lending facility.

But here is the thing: the purchasing power of the original £75,000 equivalent I borrowed way back then is today worth only £45,000. The amount of the loan may have remained the same, but inflation has eroded the value of the debt over time. Today it is worth only 60% of what it once was, while the value of the property has doubled in real terms.

None of this would have been possible if I had copied Louise’s very sensible and measured approach. Instead, I would own only that original property, which by now would probably be just about paid off.

Now before you rush out and load up on interest-only debt secured by your family home, hear some words of caution.

Firstly, interest rates will rise. Asset prices can fall. Sometimes at the same time. Seldom when convenient.

Secondly, while you may be able to postpone it for decades, eventually the loan will need to be repaid.

Thirdly, mortgages are diabolically difficult to obtain once you are no longer earning a regular pay cheque. If you do want to line up a lending facility, do it before you quit the rat race and retire!

Deploying borrowed funds to further our investing goals is not something we should be scared of. However, before we do so, we should always have a feasible plan for how we will pay them back.

Louise was justifiably proud of her achievement in paying off her home. I just wonder whether she would have been quite so happy, had she been a little better financially educated and a little less afraid of using debt as a tool.

Save the fear for things that can be neither understood nor explained.

Like my mother’s cooking.

Or the Canberra Raiders losing last weekend’s grand final.

References

- Bank of England (2019), ‘Inflation Calculator‘

- Coventry Building Society (2019), ‘Offset Flexx for Term‘

- Monevator (2019), ‘I asked the chief executive of a bank to give me a mortgage and he did‘

- OFX (2019), ‘Historical Exchange Rate‘

- Shiller, R. (2019), ‘U.S. Stock Markets 1871-Present and CAPE Ratio‘

- Vanguard (2019), ‘FTSE All-World High Dividend Yield UCITS ETF (VHYL)‘

GentlemansFamilyFinances 13 October 2019

Great post.

I went through something similar with my first company and managed to bag the redundancy.

Now freelancing and taking home a lot more than i ever believed i would.

Earning aside, the power of leverage / investment / passive income really adds up over the years.

The dirty little secret for early retirement is bagging a lifetime io mortgage when still in employment and paying it off with your 25% tax free lump sum from sipps/pensions.

That’s what i would like to do once our 5 year fixed rate comes up for renewal.

If you run the numbers and assume modest growth of investments – the difference is huge!

Plus the cash flow savings of not having to pay off somethig that could be 5 times your salary!

{in·deed·a·bly} 13 October 2019 — Post author

Thanks GFF.

Freelancing can certainly improve cash flow, but it worth remembering that the burden falls to the freelancer to fund their own benefits package. If they choose to purchase themselves a pension, private health care, and the like then the financial advantages tend to be much more modest. For mine, freelancing is more a lifestyle choice than a financial one, particularly given the risk of bench time between gigs and the inherent uncertainty. Everyone’s mileage will vary.

Using the pension lump sum is certainly one avenue for clearing down debts. Another may include selling off one asset to clear the debts encumbering assets that will be retained for cash flow. There are lots of good approaches, the important thing is to have figured out which one(s) we will apply to our own circumstances before taking on the debt in the first place.

The Rhino 13 October 2019

I hope you’re right!

My offset experiment starts in Nov, i.e. thats when the 1st payment is due.

Old property is sold as of this Wednesday.

That in itself is a huge relief as it is a buyers market down south (and it means I can now get a substantial slice of SDLT back)

So a massive financial refactor is imminent. For me that means getting into ITs and ETFs via a long dormant HL account. I’m gunning for income now – its all about replacing salaries in the lead up to a cull (but not outright extinction) of working hours.

I wish I’d found that coventry product, I think I’d have gone for that. Most likely I wouldn’t have been eligible though as mortgages are ephemeral beasts to bag in practice.

If you have shorter duration products you get headaches about keeping all your ducks in a row in the lead up to remortgaging. TI’s mentioned that in relation to his 5yr – but for him its a bit worse as its IO but not offset so he doesn’t have anywhere near the flexibility in managing that risk.

{in·deed·a·bly} 13 October 2019 — Post author

Congratulations on the property sale Rhino. The double dipping penalty on the stamp duty is huge, so is nice you manage to claw some back.

Buying control of time is an approach that has worked pretty well for me, swapping out earned income for investment income and enjoying more discretionary leisure time as a result. Hopefully you manage to strike a balance that leaves both you and the family happy and content.

That Coventry loan was interesting one, I hadn’t seen a product with a honeymoon level interest rate that wasn’t time bounded before. Hopefully it is a sign of more flexible product innovation in the marketplace.

The Rhino 14 October 2019

one thing I could pick you up on:

If you’re going to adjust for inflation on the debt, you should also adjust for inflation on the value of the asset, i.e. adjust the value downwards. Maybe you did, but you haven’t mentioned it explicitly as you did for the debt. If you haven’t inflation adjusted the asset value its probably more accurate to say its doubled rather than tripled in value. For ease, you could just not inflation adjust either value?

{in·deed·a·bly} 14 October 2019 — Post author

A fair observation Rhino, thanks for spotting the inconsistency. I’ve rephrased accordingly.

My goal was to illustrate how inflation erodes the value of debt over time. Inflation erodes purchasing power just as much on the assets side of the equation.

David Andrews 15 October 2019

Good post and many in the FI community have heated discussion regarding the wisdom of paying off the mortgage versus investing the funds. I retain an interest only offset ( it’s now fully offset as I have the same amount of funds in a linked current account ) on my first property that I’ve started renting out. It rather leaves me with a bit of a quandary. I have consent to let for 13 months and then I’ll have to discharge the mortgage fully or convert to a BTL mortgage – neither is an option I really want to take. Clearing the mortgage means I’ll have significant capital locked in the property and taking a BTL mortgage is more expensive and would reduce my yield making it less attractive to rent the property. Frustratingly it may be the case that the most “sensible” option is to not renew the tenancy and instead draw on some of the interest only funds and invest them. I’d hope that would provide a sufficient return to cover the lost rent and increased bills. I think I’m going to need a new spreadsheet.

I’m also unsure if you can get interest only offset BTL mortgages in the UK .

{in·deed·a·bly} 15 October 2019 — Post author

Thanks David.

It is possible to get buy-to-let offset mortgages. There aren’t many institutions that offer them, but some of the smaller building societies do. The buy-to-let markup on interest rates appears to be about 1%, which your otherwise forgone rental income would likely more than cover.

I’d suggest speaking to an independent mortgage broker to consider your options, they may come up with alternative approaches you haven’t yet considered. In my experience the good ones more than pay for themselves.

The Investor 25 October 2019

Ack, I missed this one when you posted it. Excellent illustration of the principles, if scantier on the risks then I’d get away with on my site. (Not saying you have under-covered the risks, I’m saying I’d be torn to shreds if I didn’t include 1,000 words on them with frequent references to the early 1990s.)

There’s a huge emotional temperament issue to all this. As you may recall I’ve been running an interest-only mortgage for a (almost) couple of years since buying my flat, which is effectively gearing up my portfolio. And I have to admit it makes me queasier than I’d like at times. I’m also *certain* it has messed with my active investing decisions (by messing with my risk tolerance, being a gateway to catastrophizing etc).

It probably hasn’t helped that it has been such a turbulent time politically, though the markets have mostly behaved. Maybe doesn’t help that the property value has dipped a bit.

We’ll see.

{in·deed·a·bly} 25 October 2019 — Post author

TI, that is quite possibly the first time I have seen somebody use the word “ack” in a written sentence. Well played sir!

You raise some astute points regarding risk, and how leverage impacts both our appetite and tolerance.

Much as we should always consider total returns when comparing investment outcomes, we should always maintain a holistic perspective of our risk exposure across our entire portfolio. Often we can be lulled into compartmentalising risk, within an account or single asset class. Using leverage is a good example of how adverse outcomes in one area of a portfolio potentially impacts several others… including our own home. Leverage may supercharge our returns, but certainly increases our risk exposure.

Your property price observation sparked a random thought. It is intriguing how many celebrate (publicly at least) a falling stock market as a buying opportunity, yet few perceive the same opportunity in a declining property market. A question of scale perhaps? Or a recognition of the difference between asset and investment? Whatever the cause, this inconsistent behaviour is fascinating to observe where cold investment theory intersects emotively with where we live.

The Investor 25 October 2019

Thanks for your further thoughts. Re: falling prices, I think it must be because most people are only ‘long’ one house at a time. And you can’t really average down into your one house as prices fall (although at least once a year — in real life, not even on my blog — I have to explain to people who are repaying their mortgage early that this is *not* what they’re doing. 🙂 )